What is a Holographic Will?

What is a holographic will? A holographic will is a handwritten will signed exclusively by the individual making the will. State laws vary regarding the legality of holographic wills. Some states recognize holographic wills only from active members of the military. Other state probate courts require two witness signatures on a holographic will to confirm…

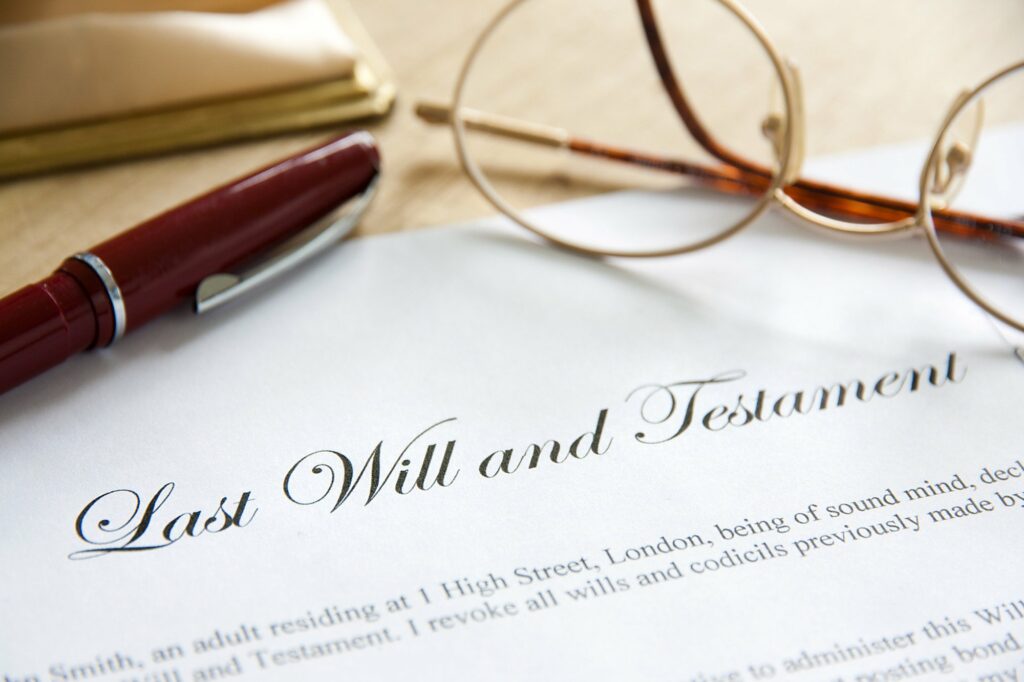

Is Your Last Will and Testament Legally Binding?

Is your last will and testament legally binding? According to a recent survey, 60% of people in the US do not have a will or a plan to make one. Accidents happen and you do not want to leave your loved ones with nothing. But your will must be legally binding if it is to be…

5 Common Mistakes When Writing a Will

There are five common mistakes when writing a will. Despite the importance of estate planning, a majority of Americans seem to neglect it. In fact, 60% of American adults do not have a will. Having more than enough to worry about already, many people do not want to add their mortality to their list of…

On The Hunt: How to Find the Best Estate Planning Lawyer

Putting together a will is something that no one wants to think about, but it is crucial when it comes to handling your wealth and finances. Planning your estate requires the help and experience of a lawyer. They will help you make sense of the process so that you and your family members are covered….

Celebrate Your Military Family, Improve Your Military Will

There’s an old military adage that says, “No good plan survives engagement.” While this quote’s timelessness must lend credit to its applicability in battle, it transcends its martial roots and applies equally as well to law. Especially Estate Law. Take for instance the idea of a Last Will and Testament. A Will is probably the…

Break Down Estate Planning By Using These Worksheets

Estate planning is not something you are probably thinking about… especially if you are decades out from retirement. It is one of those things we all know we should do but don’t think about until we are much older. Sometimes, sadly, we do not think about it until it is too late. However, regardless of…

A Young Family’s Guide to a Rock Solid Estate Plan

What does a young family need for a rock solid estate plan? If you are under 40 years old, the chances of you have thought about, or even pursuing estate planning is pretty small. However, something brought you here, and that means you are on your way to changing the way you look at planning…